In 2025, high-yield savings accounts (HYSAs) remain one of the safest and smartest ways to grow your money without taking on market risk. With the Federal Reserve cutting rates for the first time since late 2024, today’s top HYSAs—offering as much as 5.00% APY—could represent a limited-time opportunity.

Unlike traditional savings accounts from big banks, which still pay as little as 0.01% APY, high-yield savings accounts give your money the power of compounding at rates 10–12 times higher than the national average. That means even a modest deposit can earn meaningful interest over time, while keeping your funds liquid and federally insured.

Whether you’re building an emergency fund, saving for a major purchase, or simply tired of letting your cash sit idle, comparing the best HYSA rates in September 2025 can help you make the most of your savings before rates potentially decline further.

What Is a High-Yield Savings Account?

A high-yield savings account (HYSA) is a type of deposit account offered by banks and credit unions that pays a much higher interest rate than a standard savings account. While traditional savings accounts at major banks may offer 0.01% to 0.10% APY, high-yield savings accounts often pay 4.00%–5.00% APY or more, depending on the institution and market conditions.

The main reason for this difference is that many HYSAs are offered by online banks and fintech institutions. Without the overhead costs of physical branches, they can pass more of their profits to customers in the form of higher interest rates.

Key Features of HYSAs

- Competitive Interest Rates – Earn several times more interest than with a standard savings account.

- Safety – Deposits are typically insured by the FDIC (for banks) or NCUA (for credit unions) up to $250,000 per depositor, per institution.

- Liquidity – Funds are accessible, though federal law may limit certain withdrawals or transfers to six per month.

- Low or No Minimums – Many HYSAs require little to no minimum deposit, making them accessible to everyday savers.

- Online Banking Access – Most accounts include mobile apps, online dashboards, and convenient ACH transfers.

How HYSAs Differ From Other Accounts

- Traditional Savings Accounts – Lower APY, more branch access.

- Money Market Accounts – Often include check-writing privileges but may require higher balances.

- Certificates of Deposit (CDs) – Lock in rates for a fixed term but reduce liquidity.

In short, a high-yield savings account is best for people who want a safe, flexible place to park cash while still earning meaningful interest.

Top High-Yield Savings Accounts (September 2025 Update)

The table below highlights some of the best high-yield savings accounts in September 2025, comparing APYs, minimum deposits, and standout features.

Comparison Table

| Institution | APY | Minimum Deposit | Balance Requirement | Best For |

|---|---|---|---|---|

| Varo Bank | 5.00% | $0 | $0 (up to $5k) | Best Overall |

| AdelFi Credit Union | 5.00% | $25 | $0 (new members only) | Faith-based CU |

| Fitness Bank | 4.75% | $100 | $100 + 10k steps/day | Fitness-focused savers |

| Axos Bank | 4.46% | $0 | $1,500 | Digital convenience |

| Vibrant CU | 4.50% | $0 | $0 (<$15k) | Low-balance savers |

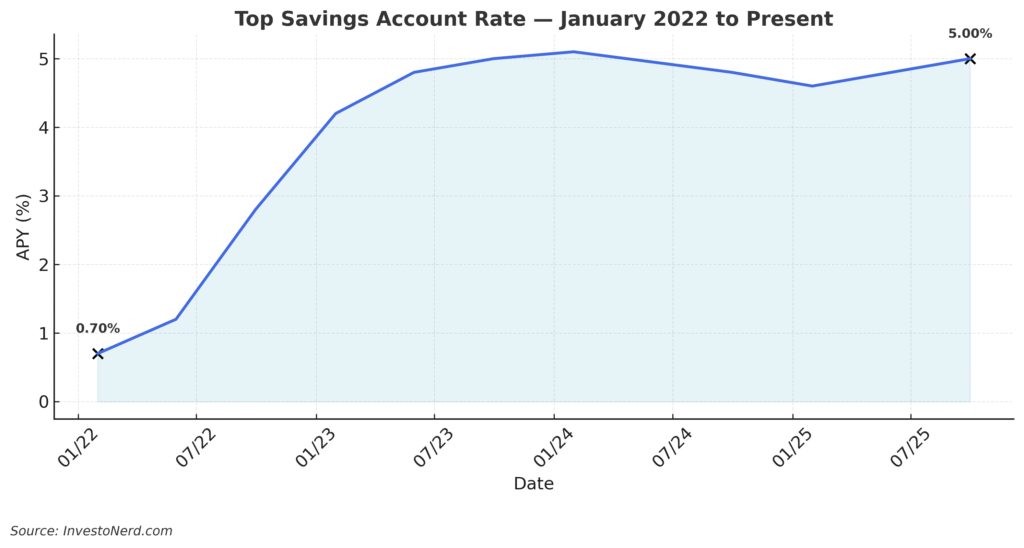

Since January 2022,

the top nationally available savings account rate has climbed from under 1% before the Fed’s March 2022 rate hikes, peaked above 5.5% in 2024, and has begun easing following the rate cuts that started in September 2024.

Account Highlights

1. Varo Bank – Best Overall

Varo consistently ranks among the best thanks to its 5.00% APY on balances up to $5,000. No monthly fees, no minimum deposit, and a sleek mobile app make it a top pick for everyday savers. However, balances above $5,000 earn a lower rate, so it’s ideal for small-to-medium savers.

2. AdelFi Credit Union – Best for Faith-Based Banking

AdelFi offers 5.00% APY for new members with just a $25 minimum deposit. While it requires membership (faith-based), its competitive rate and low entry point make it a strong choice for those who qualify.

3. Fitness Bank – Best for Active Lifestyles

This account is unique: earn up to 4.75% APY if you maintain an average of 10,000 steps per day (tracked through their mobile app). Perfect for those who want to combine healthy living with financial rewards.

4. Axos Bank – Best Digital Bank Experience

Axos offers 4.46% APY with no deposit requirement, but to earn the full rate you must meet monthly activity requirements (like having direct deposits and 10 debit card transactions). Great for tech-savvy users who want an all-in-one digital banking solution.

5. Vibrant Credit Union – Best for Low Balances

With 4.50% APY on balances under $15,000, Vibrant CU is excellent for those just starting to save. There’s no minimum balance requirement, and the account is straightforward with few conditions.

How Much You Can Earn With a High-Yield Savings Account

One of the biggest advantages of a high-yield savings account is seeing your money grow passively without market risk. The difference in earnings compared to a traditional savings account can be dramatic.

Let’s break it down with some realistic examples using an average 5.00% APY vs. a 0.40% APY (typical at large banks in 2025).

Potential Earnings Over 1 Year

| Deposit Amount | Earnings at 5.00% APY | Earnings at 0.40% APY | Extra Earned in HYSA |

|---|---|---|---|

| $1,000 | $50.00 | $4.00 | $46.00 |

| $5,000 | $250.00 | $20.00 | $230.00 |

| $10,000 | $500.00 | $40.00 | $460.00 |

| $50,000 | $2,500.00 | $200.00 | $2,300.00 |

Assumes interest is compounded monthly and the APY remains constant over the year.

Why This Matters

- With just $10,000, the difference between a HYSA and a traditional savings account is nearly $460 in one year.

- For larger balances, like $50,000, the gap grows into thousands of dollars.

- Unlike investments in stocks or bonds, this growth is risk-free and FDIC/NCUA insured (up to $250,000).

Tip: Even if rates fall later in 2025, locking in a HYSA today means you start earning immediately—and every month your money sits idle at a traditional bank, you’re losing potential interest.

Pros & Cons of High-Yield Savings Accounts

Like any financial product, high-yield savings accounts come with both benefits and limitations. Understanding these can help you decide whether an HYSA is the right place for your money.

Pros

- Higher Interest Rates

- Earn significantly more than traditional savings accounts—often 10–12 times the national average.

- Safety & Security

- Deposits are insured by the FDIC (banks) or NCUA (credit unions) up to $250,000 per depositor, per institution.

- Liquidity

- Funds remain accessible; you can transfer money back to your checking account as needed.

- Low Barriers to Entry

- Many HYSAs have no minimum deposit and no monthly fees, making them ideal for beginners.

- Great for Short-Term Goals

- Perfect for emergency funds, vacation savings, or down payment funds where safety matters more than high risk/high reward.

Cons

- Variable Rates

- APYs can fluctuate depending on market conditions and Fed policy. Today’s 5.00% may not last forever.

- Balance Caps

- Some accounts pay the highest APY only up to a certain balance (e.g., $5,000 or $10,000).

- Withdrawal Limits

- Federal Regulation D (though relaxed during COVID-19) still allows banks to limit certain withdrawals to 6 per month.

- Online-Only Banking

- Many HYSAs are offered by digital banks, which means no physical branches for in-person service.

- Not a Long-Term Investment

- While safe, HYSAs don’t offer the long-term growth potential of stocks, ETFs, or retirement accounts.

Bottom line: High-yield savings accounts are excellent for safety and short-term savings goals, but not a substitute for long-term investing.

Alternatives to High-Yield Savings Accounts

While HYSAs are one of the safest and most flexible ways to earn on your cash, they’re not the only option. Depending on your financial goals, you may find better fits in one of these alternatives:

1. Certificates of Deposit (CDs)

- What it is: A fixed-term deposit where you agree to leave your money for a set period (3 months, 12 months, 5 years, etc.) in exchange for a guaranteed interest rate.

- Pros:

- Often slightly higher rates than HYSAs.

- Fixed returns = predictability.

- Cons:

- Limited liquidity—you pay a penalty for early withdrawal.

- Best for: Savers who don’t need access to their money for a defined time.

2. Money Market Accounts (MMAs)

- What it is: A savings product that sometimes offers check-writing and debit card access.

- Pros:

- Similar APYs to HYSAs.

- Added flexibility with check access.

- Cons:

- Higher minimum balance requirements.

- Best for: People who want savings growth with limited transactional features.

3. Rewards Checking Accounts

- What it is: Checking accounts that pay high interest if you meet conditions like using your debit card 10+ times per month.

- Pros:

- Rates can exceed even the best HYSAs (sometimes 5%+ APY).

- No withdrawal restrictions like savings accounts.

- Cons:

- Must meet activity requirements or APY drops dramatically.

- Best for: Active spenders who use their checking account daily.

4. Short-Term Bond Funds

- What it is: Investment funds holding government and corporate bonds with short maturities.

- Pros:

- Potentially higher yields than savings accounts.

- Still relatively low risk compared to stocks.

- Cons:

- Not FDIC-insured.

- Value can fluctuate with interest rate changes.

- Best for: Savers willing to accept mild risk for better returns.

5. Treasury Bills (T-Bills)

- What it is: U.S. government debt securities that mature in less than a year.

- Pros:

- Backed by the U.S. government = ultra-safe.

- Competitive yields, often on par with top HYSAs.

- Cons:

- Funds locked until maturity (unless sold on the secondary market).

- Best for: Conservative investors who want government-backed safety.

In short: If you prioritize flexibility, HYSAs are unbeatable. If you’re okay sacrificing liquidity, CDs or T-bills might offer slightly better returns.

How to Choose the Right High-Yield Savings Account

Not all high-yield savings accounts are created equal. The “best” account for you depends on your savings goals, balance size, and banking preferences. Here are the key factors to consider before opening one:

1. Annual Percentage Yield (APY)

- The higher the APY, the faster your money grows.

- Compare current rates but also check whether the APY is introductory (temporary) or ongoing.

2. Minimum Deposit Requirements

- Some banks let you open an account with $0, while others may require $100–$1,000 to start.

- Choose one that fits your budget.

3. Balance Caps

- Many HYSAs pay their top APY only on balances up to a certain threshold (e.g., $5,000 or $10,000).

- If you plan to deposit a larger sum, check how the bank treats amounts above the cap.

4. Fees and Penalties

- Most online banks offer fee-free savings, but some charge for excessive withdrawals or account inactivity.

- Always read the fine print to avoid surprises.

5. Access and Usability

- Does the bank offer a strong mobile app, easy transfers, and 24/7 support?

- Consider whether you’re comfortable with online-only banking or prefer having a branch nearby.

6. FDIC/NCUA Insurance

- Confirm that the institution is federally insured up to $250,000 per depositor, per institution.

- This guarantees your money is safe even if the bank fails.

7. Special Features

- Some accounts offer perks like ATM access, goal trackers, or step-based rewards (e.g., Fitness Bank).

- Pick one that aligns with your lifestyle.

Example: Matching Accounts to Needs

| Saver Type | Best Choice | Why |

|---|---|---|

| Beginner saver | Varo Bank | No minimums, easy app |

| Large balance holder | Axos Bank / CDs | Higher limits, better for >$10k |

| Active lifestyle saver | Fitness Bank | Step-based rewards |

| Tech-savvy user | Axos Bank | Full digital banking |

| Low-balance saver | Vibrant Credit Union | High APY for under $15k |

Pro Tip: Don’t just chase the top advertised APY. Consider how you’ll actually use the account—sometimes convenience and flexibility outweigh a slightly higher rate.

Step-by-Step Guide to Opening a High-Yield Savings Account

Opening a high-yield savings account is usually quick and fully online. Here’s a simple roadmap to get started:

1. Compare Options

- Review APYs, fees, and requirements.

- Narrow down 2–3 banks or credit unions that best fit your needs.

2. Check Eligibility

- Some institutions are nationwide, while others (like credit unions) may require membership based on geography, employer, or affiliation.

- Confirm you qualify before applying.

3. Gather Required Documents

You’ll need basic personal information, such as:

- Full name, date of birth, Social Security number (SSN) or Tax ID

- A valid government-issued ID (driver’s license, passport, etc.)

- Proof of address (utility bill or lease, in some cases)

4. Complete the Online Application

- Fill out the bank’s form with your details.

- Some banks may ask security questions for identity verification.

5. Fund Your Account

Common funding options include:

- ACH transfer from another bank account

- Debit card deposit

- Wire transfer

- Check deposit (mobile or mailed)

Many banks allow you to start with as little as $0–$25.

6. Set Up Recurring Deposits

- Automating contributions helps you build savings effortlessly.

- Example: $200/month automatically transferred = $2,400 saved in a year, not counting interest.

7. Activate Online & Mobile Banking

- Download the bank’s mobile app.

- Set up account alerts for deposits, withdrawals, or APY changes.

Expert Insights & Financial Advisor Tips

To make the most of a high-yield savings account, it helps to think like a financial planner. Here are some insights based on what advisors often recommend:

1. Use HYSAs for Short-Term Goals Only

“A high-yield savings account is ideal for money you’ll need within 1–3 years. Think of it as a parking spot for your cash, not a long-term investment vehicle.”

— Certified Financial Planner (CFP)

Examples: emergency fund, vacation savings, wedding fund, home down payment.

2. Don’t Chase Rates Too Aggressively

“It’s tempting to jump banks for an extra 0.10% APY, but unless you’re holding a very large balance, the difference may be just a few dollars a year. Focus on reliability and convenience too.”

— Personal Finance Coach

3. Pair HYSAs With Other Products

“Smart savers often split funds—keeping their emergency fund in a HYSA while investing long-term money in retirement accounts or index funds. This way, they balance safety with growth.”

— Wealth Advisor

4. Watch Out for Rate Drops

Since APYs are variable, they can decline when the Federal Reserve cuts rates.

Pro Tip: If you’re worried about falling rates, consider opening a short-term CD to lock in today’s returns while still keeping part of your savings liquid in an HYSA.

5. Automate Savings to Stay Consistent

Building wealth is less about chasing the perfect APY and more about forming consistent habits. Set up automatic transfers so you don’t have to rely on willpower.

Over the past 18 months, Americans have saved an average of about 4%–4.5% of their disposable (after-tax) income.

Frequently Asked Questions (FAQs) About High-Yield Savings Accounts

1. Are high-yield savings accounts safe?

Yes. As long as the bank is FDIC-insured (or NCUA-insured for credit unions), your deposits are protected up to $250,000 per depositor, per institution.

2. Do HYSA rates change?

Yes. Rates are variable and depend on market conditions. If the Federal Reserve lowers interest rates, banks often follow by reducing APYs.

3. Can I have more than one HYSA?

Absolutely. Many people open multiple HYSAs for different goals (emergency fund, vacation savings, home down payment). Just keep total balances under the FDIC/NCUA insurance limits per institution.

4. Are HYSA earnings taxable?

Yes. Any interest earned is considered taxable income and must be reported on your tax return, even if you don’t withdraw it. Banks typically send you a Form 1099-INT if you earn more than $10 in interest in a year.

5. How do I access money in a HYSA?

You can usually transfer funds electronically to a linked checking account. Some banks

Frequently Asked Questions (FAQs) About High-Yield Savings Accounts

1. Are high-yield savings accounts safe?

Yes. As long as the bank is FDIC-insured (or NCUA-insured for credit unions), your deposits are protected up to $250,000 per depositor, per institution.

2. Do HYSA rates change?

Yes. Rates are variable and depend on market conditions. If the Federal Reserve lowers interest rates, banks often follow by reducing APYs.

3. Can I have more than one HYSA?

Absolutely. Many people open multiple HYSAs for different goals (emergency fund, vacation savings, home down payment). Just keep total balances under the FDIC/NCUA insurance limits per institution.

4. Are HYSA earnings taxable?

Yes. Any interest earned is considered taxable income and must be reported on your tax return, even if you don’t withdraw it. Banks typically send you a Form 1099-INT if you earn more than $10 in interest in a year.

5. How do I access money in a HYSA?

You can usually transfer funds electronically to a linked checking account. Some banks also allow ATM access or debit cards, though HYSAs are not meant for daily spending.

6. Is there a limit to withdrawals?

Yes, but it depends on the bank. Many limit you to six certain transfers/withdrawals per month (a carryover from Regulation D). Exceeding this may result in fees or account closure.

7. What’s the difference between APY and interest rate?

- Interest rate = the base rate the bank pays.

- APY (Annual Percentage Yield) = includes compounding, giving you a more accurate measure of your actual earnings.

Conclusion: Why a High-Yield Savings Account Still Matters in 2025

In a financial world full of complex investments, high-yield savings accounts stand out for their simplicity, safety, and steady growth. With top APYs still hovering near 5.00% in September 2025, they provide an excellent way to make your idle cash work harder—especially compared to traditional savings accounts that pay close to nothing.

Whether you’re building an emergency fund, saving for a big purchase, or just looking to beat inflation without risk, a HYSA can be a powerful tool in your financial toolkit.

But remember:

- HYSAs are not long-term investment vehicles. For retirement and wealth-building, you’ll want to consider stocks, ETFs, or retirement accounts.

- Rates are variable, so take advantage of today’s high APYs while they last.

- The “best” HYSA isn’t always the one with the highest advertised rate—look for accounts that fit your lifestyle, balances, and access needs.

Bottom line: If you haven’t already opened a high-yield savings account, now is the time. The earlier you start, the more interest you’ll earn—risk-free.

Simplifying finance with clear insights on credit, loans, insurance, and investing – InvestoNerd.

Realted Article

- Top Economist Warns: Rising Inflation and Slowing Growth Are Investors’ Worst Nightmare

- Best High-Yield Savings Accounts in September 2025: Maximize Your Cash While Rates Last

- Investing: An Introduction

- How To Start Investing in Stocks in 2025 and Beyond

- The 10 Richest People in the World (September 2025 Update)

- How Do I Keep Commissions and Fees From Eating Trading Profits?

- 4 Basic Things to Know About Bonds

- What Are Stock Fundamentals?